Note: The restrictions imposed by the Model Code of Conduct delayed the 15th FC’s work, causing it to complete its state visits later than expected. As a result, its detailed assessment of different states’ requirements was affected. To address this, the Union Cabinet extended the term of the 15th FC by one year. Consequently, the Commission submitted two reports—one for the fiscal year 2020-21 and another covering the financial years 2021-22 to 2025-26.

Functions of the FC

The terms of reference defined by each commission govern the function it is tasked with carrying out. These Terms of Reference (ToR), derived from Article 280(3) of the Indian Constitution, require the Finance Commission to provide recommendations to the government on key financial matters. These include: i) Deciding how much of the Centre’s tax revenue should go to the States (vertical sharing). ii) Determining each State’s share in the total pool of Central taxes (horizontal distribution). iii) Recommending Grants-in-Aid to states that require financial support for their revenues. iv) Suggest ways to strengthen the Consolidated Fund of States to help Panchayats and Municipalities with additional resources. v) Under Article 280(2)(c), the President can assign any other financial matters to the Commission if necessary for better fiscal management. These include improving government efficiency and transparency in administration, as well as creating financial plans to support states during emergencies, such as natural disasters.

In this article, we will focus on two key functions: 1. Tax devolution and 2. Grants-in-aid of the revenues of the States.

Tax Devolution

A key responsibility of the Finance Commission (FC), as outlined in Article 280(3)(a) of the Constitution, is tax devolution. This refers to the FC’s role in recommending how tax revenues should be distributed between the central government and the state governments. The word devolution refers to the process by which a central government transfers specific political powers to smaller government bodies, such as regional or local governments. It is the most important function of the FC, as tax devolution is the primary means through which the Centre transfers resources to the states. Tax devolution is carried out in two steps: 1) Vertical devolution and 2) Horizontal devolution.

The FC determines the proportion of the Centre’s net tax revenue to be shared with the States. This share, known as the divisible pool, includes taxes such as corporation tax, personal income tax, Customs duty, Central Goods and Services Tax (CGST), and the Centre’s share of Integrated Goods and Services Tax (IGST). However, cesses and surcharges, which made up about 28% of the Centre’s gross tax revenue in 2021–22, are excluded from the divisible pool and remain with the Centre. This allocation of tax revenue between the Centre and the States is known as vertical devolution. Once the total share of states (tax devolution + grants) from the divisible pool is decided, the FC determines how much each state will receive through a process called horizontal devolution. To ensure a fair distribution among all 28 states, the FC allocates shares based on specific parameters, which are broadly grouped into need-based, equity-based, and performance-based criteria.

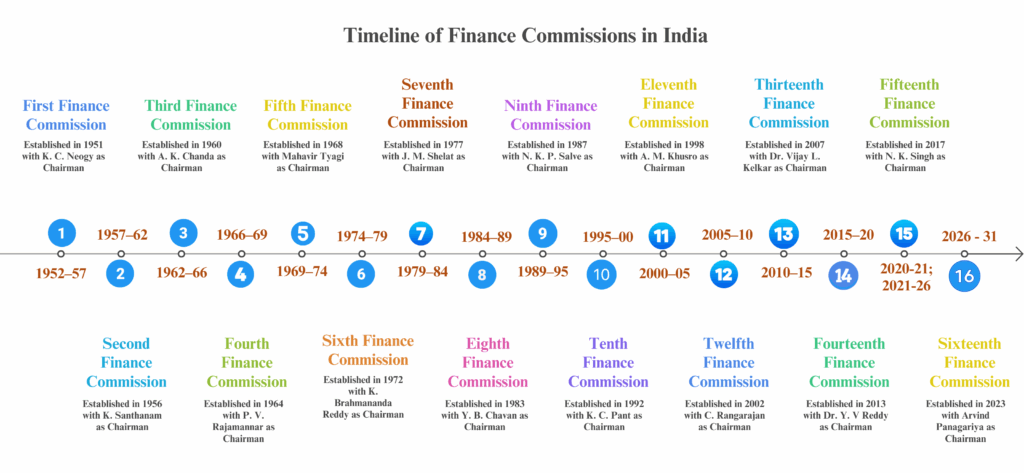

Up to the 10th FC, the states’ share from the Centre’s tax revenue was determined based on Personal Income Tax and Union Excise Duties. The First Finance Commission had recommended that 55% of income tax revenues and 40% of Union excise duties be shared with the states. As the expenditure responsibilities of states expanded over time, their share in the net proceeds of Union taxes also increased. Recognising the need for greater stability and buoyancy in transfers, the 11th FC recommended that states should benefit from the entire range of Central taxes rather than only select ones. It recommended that 29% of the aggregate central tax revenues be shared with the states.

Acting on this principle, the 81st Constitutional Amendment (2000) brought about a fundamental change in the sharing pattern of Union taxes. The amendment revised Article 270 to include all Central taxes and duties, except those mentioned in Articles 268, 269, and 269A, along with surcharges and cesses levied for specific purposes, within the divisible pool to be shared with the states. This reform ensured that states could enjoy a predictable and buoyant flow of resources linked to the overall growth of Central tax revenues.

Table 2: States’ Share in Central Taxes Across Finance Commissions

| Finance Commission (Period) | State’s Share in Net Proceeds of | ||

| Income Tax (%) | Union Excise Duties (%) | All Shareable Union Taxes (%) | |

| FC-1 (1952-57) | 55 | 40 | |

| FC-2(1957-62) | 60 | 25 | |

| FC-3(1962-66) | 66.66 | 20 | |

| FC-4(1966-69) | 75 | 20 | |

| FC-5(1969-74) | 75 | 20 | |

| FC-6(1974-79) | 80 | 20 | |

| FC-7(1979-84) | 85 | 40 | |

| FC-8(1984-89) | 85 | 45 | |

| FC-9-I(1989-90) | 85 | 40 | |

| FC-9-II(1990-95) | 85 | 45 | |

| FC-10(1995-00) | 77.5 | 47.5 | |

| FC-11(2000-05) | 29.5 | ||

| FC-12(2005-10) | 30.5 | ||

| FC-13(2010-15) | 32 | ||

| FC-14(2015-20) | 42 | ||

| FC-15-I(2020-21) | 41 | ||

| FC-15-II(2021-26) | 41 | ||

Source: Finance Commission Reports

For the 2021–26 period, total transfers to the states, including ₹42.2 lakh crore through tax devolution and₹10.33 lakh crore in grants, are estimated to remain around 50.9% of the divisible pool (103 lakh crore).

While considering total resource transfers to states, tax devolution has consistently formed the major component. Since the 1st FC, on average, over 84% of the transfers recommended by the 1st to the 12th FCs have been through tax devolution.

The share of tax devolution has fluctuated significantly over the years. For instance, in the 6th FC (1974-79), only 73.9% of total transfers were allocated through tax devolution. This figure saw a substantial increase in the 7th FC (1979-84), where the share rose to 92.2%. However, in the following years, the tax devolution percentage declined. The 11th FC recommended 86.5% of transfers through tax devolution, and more recently, the 15th FC suggested a share of 80.3%.

Grants-in-Aid

Based on the FC’s recommendations, states receive grants-in-aid of the revenues of the States from the Centre to support development projects or address revenue shortfalls. Under Article 275 of the Constitution, the FC is responsible for recommending both the principles and the amount of grants for states in need of financial assistance. These transfers help bridge financial gaps and promote equitable development by targeting specific states or sectors in need of support or reform.

These grants are allocated from the Consolidated Fund of India, the government’s primary account that holds all revenues, including taxes and loans, for expenses such as state grants. Grants are of two types: tied and untied. Tied grants come with specific conditions, restricting their use to designated areas or purposes. In contrast, untied grants provide states with the flexibility to allocate funds according to their own needs and priorities without restrictions. For example, out of the total grants earmarked for Panchayati Raj institutions, 60% are tied and allocated for national priorities such as drinking water supply, rainwater harvesting, and sanitation. In contrast, 40% are untied, allowing Panchayati Raj institutions to use them at their discretion for improving basic services.

It is important to note that grants-in-aid of the revenues of the States are distinct from the divisible pool, as they are not part of it.

Grants-in-aid of the revenues have fluctuated significantly over time. Under the Sixth FC (1974-79), they accounted for 26.1% of total transfers, but this dropped sharply to 7.7% under the 7th FC (1979-84). The 12th FC (2005-10) experienced a rebound, with grants accounting for 18.9% of total transfers. For the 15th FC (2021–26), grants are 19.6% of total transfers. These shifts are influenced by economic conditions, the central government’s financial health, tax revenue trends, and political dynamics. Note that the operational period of the 6th FC (1974-79) coincided with pre-emergency and emergency years, while the 7th FC was established during the tenure of the first non-Congress government in the aftermath of the emergency.

Table 3: Grants in aid vs. tax devolution (% of total Finance Commission Transfers)

Source: NIPFP Report

Grants from the Centre to states are of two types: statutory and discretionary.

-

- Statutory Grants: Article 275 allows Parliament to provide financial grants to states that need assistance. The amount of these grants can vary each year and is taken from the Consolidated Fund of India, based on the recommendations of the FC. The reason these are called Statutory Grants is that they are sanctioned by a specific parliamentary law.

- Discretionary Grants: Article 282 allows both the Centre and states to provide discretionary grants for public purposes beyond their legislative competence. These grants, allocated based on need, priority, or emerging situations, typically lack a fixed formula and are often substantial. They enable states to meet plan targets while giving the Union Government leverage to align state policies with national priorities. Discretionary transfers, often linked to centrally sponsored schemes (CSS) or special projects, grant the Centre significant control over fund distribution. Previously, the Planning Commission played a key role in recommending such grants, particularly in the early years after independence, when they often exceeded statutory allocations.

The following grants are generally provided to states from the centre’s resources:

-

- Revenue Deficit Grants: To eliminate revenue deficits of the state.

-

- Grants to Local Bodies: For local development and health initiatives, often with performance-linked conditions.

-

- Disaster Risk Management Grants: For disaster preparedness and response.

-

- Sector-Specific Grants: Focused on health, education, agriculture, roads, judiciary, and more.

-

- State-Specific Grants: Addressing the unique needs of each state, such as infrastructure or social services.

Revenue deficit grants and local government grants together constitute the majority of FC grants. They accounted for around 90% under the 14th FC, followed by about 71% under the 15th FC.

Table 4: Grants for 2021-26 (15th FC) (Rs crore)

| Grants | Revenue deficit grants | Local governments grants | Disaster management grants | Sector-specific grants | State-specific grants | Total |

|---|---|---|---|---|---|---|

| Amount | 294514 | 436361 | 122601 | 129987 | 49599 | 1033062 |

*Note: The table is provided as an example to give readers an overview of how the grants are distributed.

Interestingly, the Constitution also provided for a special type of grants-in-aid of the state’s revenues under Article 273 for a temporary period after India’s independence. For a decade (until 1960), states that grew jute, such as West Bengal, Bihar, Orissa, and Assam, received grants-in-aid from the Union. These grants were linked to the export duty on jute products, offering financial support based on the export of jute.

The FC undeniably plays a pivotal role in shaping India’s fiscal federalism through its structured approach to resource distribution. In a country with vast geography, regional disparities, and diverse needs across states, its responsibility in maintaining a balance between the Centre and the states while promoting fiscal discipline is commendable.

However, in recent years, the distribution framework adopted by the Commission has faced increasing challenges, particularly from the southern states. In the next article, we will examine one of the core conflicts that has emerged — the formula designed by the 15th FC for allocating taxes among states.

Ishant Deshmukh, Research Assistant, JP-SSSC

If you want to communicate with us, kindly write to [email protected]